May 7, 2025

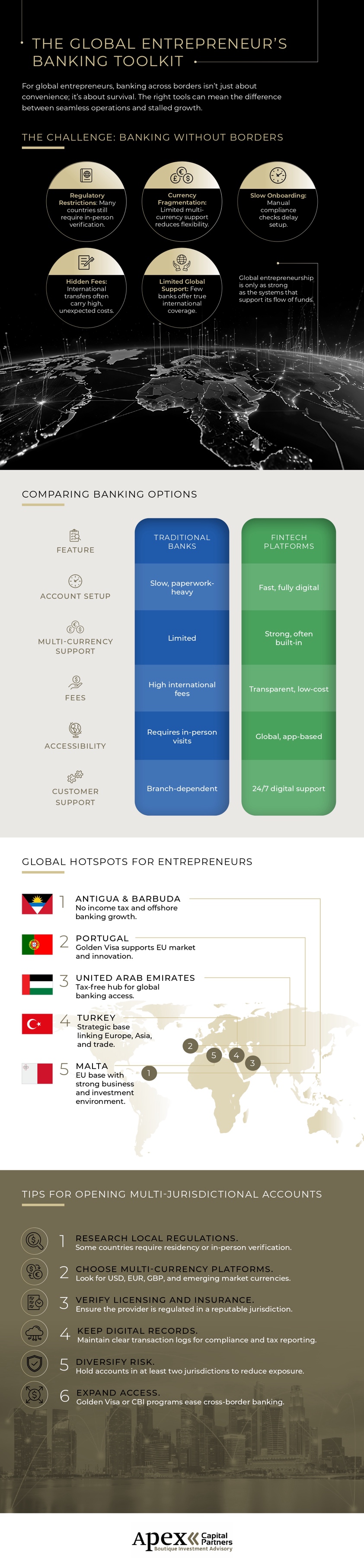

Running a business across borders requires more than a standard checking account. Global entrepreneurs often deal with international payments, currency changes, tax records, vendor relationships, and banking rules in more than one country. Having the right banking tools in place can help business owners manage money with greater control, reduce delays, and support growth in new markets.

A multi-currency account can make international business easier to manage. These accounts allow entrepreneurs to receive, hold, and send money in different currencies. This can reduce the need to convert funds every time a payment arrives. It may also help business owners plan around exchange rates and avoid unnecessary fees.

Fast payment processing matters when business activity crosses borders. Entrepreneurs should choose payment systems that support international transfers, digital invoices, and multiple payment methods. Customers may prefer credit cards, bank transfers, mobile wallets, or local payment options depending on where they live. Clear payment systems can reduce late payments and improve customer experience. They also make it easier to track revenue by region or client type.

Global businesses often have expenses in several currencies. Travel, software, shipping, contractors, taxes, and vendor payments can become difficult to manage without organized records. Business credit cards, digital receipts, and accounting software can help track spending more clearly.

Accurate expense records also support tax preparation and financial planning. Entrepreneurs should review reports regularly to identify rising costs or payment issues before they create larger problems.

Growth often requires additional funding. Global entrepreneurs may need credit lines, business loans, equipment financing, or trade finance to support expansion. Access to funding can help cover inventory, payroll, marketing, or new market entry costs.

Business owners should compare interest rates, repayment terms, fees, and qualification requirements before choosing financing. A strong banking relationship may also make it easier to secure support when the business is ready to grow.

International banking often involves strict documentation rules. Banks may request business registration documents, tax records, ownership details, contracts, and proof of business activity. Keeping these records organized can reduce delays when opening accounts or completing large transactions. Entrepreneurs should also stay aware of reporting requirements in countries where they operate.

Some business owners reviewing global mobility options, including citizenship by investment programs, may also need to consider how residence, banking access, and tax planning connect to long-term business strategy.

Global banking requires strong security habits. Two-factor authentication, secure passwords, transaction alerts, and account permission controls can help protect business funds. Entrepreneurs should also limit account access to trusted team members and review permissions regularly.

Banking tools are an important part of building a global business. Multi-currency accounts, reliable payment systems, expense tracking, financing access, compliance records, and security practices all help entrepreneurs operate with more confidence. With the right toolkit, business owners can manage international growth more efficiently and make stronger financial decisions across markets.

The core toolkit includes multi-currency accounts, reliable payment systems, strong expense tracking, access to financing, compliance documentation, and digital security controls.

It lets a business receive, hold, and send money in different currencies, reducing constant conversions and helping owners plan around exchange rates and fees.

Organized records across currencies support tax preparation and financial planning, and regular reviews surface rising costs or payment issues early.

Banks often request business registration, tax records, ownership details, contracts, and proof of activity, so keeping these organized reduces delays.

Two-factor authentication, secure passwords, transaction alerts, limited account access, and regular permission reviews all help protect funds.